|

Yesterday Part 1 laid out the empirical record on the packer tier: ten quarters of Tyson Beef segment losses totaling roughly $2.08 billion, JBS Beef North America swinging $566 million year over year to a $319.5 million loss, cow-calf returns at the strongest level in industry history, and a United States beef cow herd at its lowest level since 1961. If the packer is not extracting the consumer dollar, something else is. Today we show you what the data say it is.

The argument in one paragraph

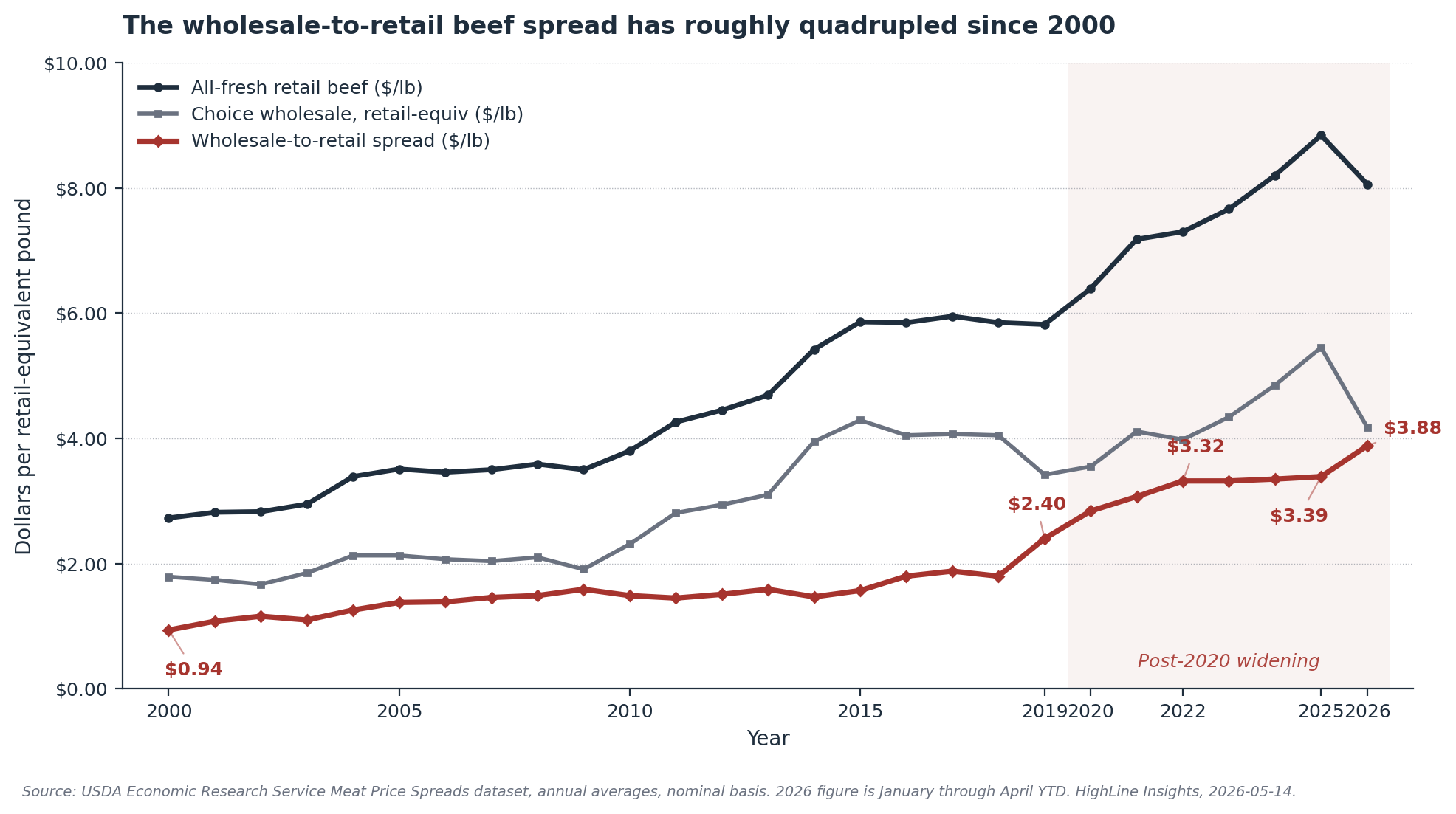

The wholesale-to-retail beef spread, the gap between what the packer sells boxed beef for and what the supermarket charges at the case, has roughly quadrupled in nominal terms since 2000. The most aggressive widening occurred after 2020, the same window in which packer beef segments collapsed into accelerating losses. The retail tier is itself concentrated, with the top five grocery chains controlling roughly 48 percent of United States food-at-home sales. Pass-through from wholesale to retail is empirically asymmetric: shelf prices rise quickly when boxed beef rises and fall slowly, or not at all, when boxed beef falls. Each of those three facts is documented in USDA Economic Research Service data, USDA published research, and peer-reviewed agricultural economics literature. Together they describe the part of the consumer beef price system the DOJ investigation is not examining.

1. The Spread Itself: 2000 to 2026 YTD

The cleanest reference is the USDA ERS Meat Price Spreads dataset, which has tracked the all-fresh retail value, the wholesale value, the net farm value, and the gross farm-to-retail spread on a monthly basis since 1970. ERS converts both wholesale and retail to a common per-pound retail-equivalent basis using a 1.14 lb wholesale to 1 lb retail conversion factor. All values in the chart below are nominal.

|

|

Source: USDA Economic Research Service Meat Price Spreads dataset, annual averages, nominal basis. 2026 figure is January through April YTD.

|

Three structural facts emerge from the series.

First, the gross spread has roughly quadrupled in nominal terms. $0.94 per retail-equivalent pound in 2000. $3.39 per pound in 2025. $3.88 per pound through April 2026, a fresh nominal high. The trajectory is not noise around a trend. It is a level shift, with two visible inflection windows.

Second, the spread widened most aggressively in two windows: 2014 through 2016, and 2020 forward. The 2014 to 2016 window tracked the historic feeder cattle peak and the supply shock that followed BSE-era herd contraction. The post-2020 window is the one that matters for today’s policy debate, because it is the window the current investigation is implicitly framed around.

Third, the recent five-year stretch is unambiguous. Between 2019 and 2025, Choice cutout on a retail-equivalent basis climbed from $3.42 per pound to $5.45 per pound, roughly a 60 percent increase. Over the same period, all-fresh retail beef moved from $5.82 per pound to $8.84 per pound, roughly a 52 percent increase. In absolute per-pound terms, wholesale added $2.03 per pound while retail added $3.02 per pound. The spread itself rose from $2.40 per pound to $3.39 per pound, a 41 percent expansion of the gross margin between the packer’s selling price and the supermarket’s posted shelf price.

The COVID-era illustration is the cleanest single piece of evidence in the series. In 2020, wholesale on a full-year average basis was only modestly higher than 2019, but retail jumped from $5.82 per pound to $6.39 per pound and never gave back the gain. The shelf price became the new floor. The far more diagnostic year is 2022. With the cutout falling year over year, retail nonetheless climbed from $7.18 per pound to $7.30 per pound. The spread widened to $3.32 per pound, the highest level on record at that time. In other words, in 2022 the packer’s gross share of the consumer dollar was shrinking while the retailer’s share was growing.

|

In 2022, the cutout fell. Retail rose. The spread widened to a record. That is not a packer-driven price story.

|

One honest caveat. The spread is a gross figure, not a retailer net margin. It absorbs grocer labor, refrigeration, shrinkage, advertising, and category management overhead before any operating profit attaches at the case level. No single line item in the widening can be assigned to any one cause. But the size of the move, $2.94 per pound of nominal expansion in twenty-six years, and the persistence of the post-2020 widening through wholesale softening, points the empirical record at the retail channel rather than the slaughter and fabrication stage.

2. The Tier the DOJ Is Not Examining: Retail Concentration

Start with the empirical contrast. USDA data put fed steer and heifer slaughter at roughly 85 percent CR4 for the four publicly identified beef packers. That figure is real, and it is the figure the May 4 press conference anchored on. It is also incomplete as a description of the consumer beef price system, because consumers do not buy boxed beef at the cutout. They buy ground chuck and ribeye at a grocery shelf. The variable that determines whether wholesale-side changes reach the household budget is the retail margin, set by a separately concentrated tier of the supply chain.

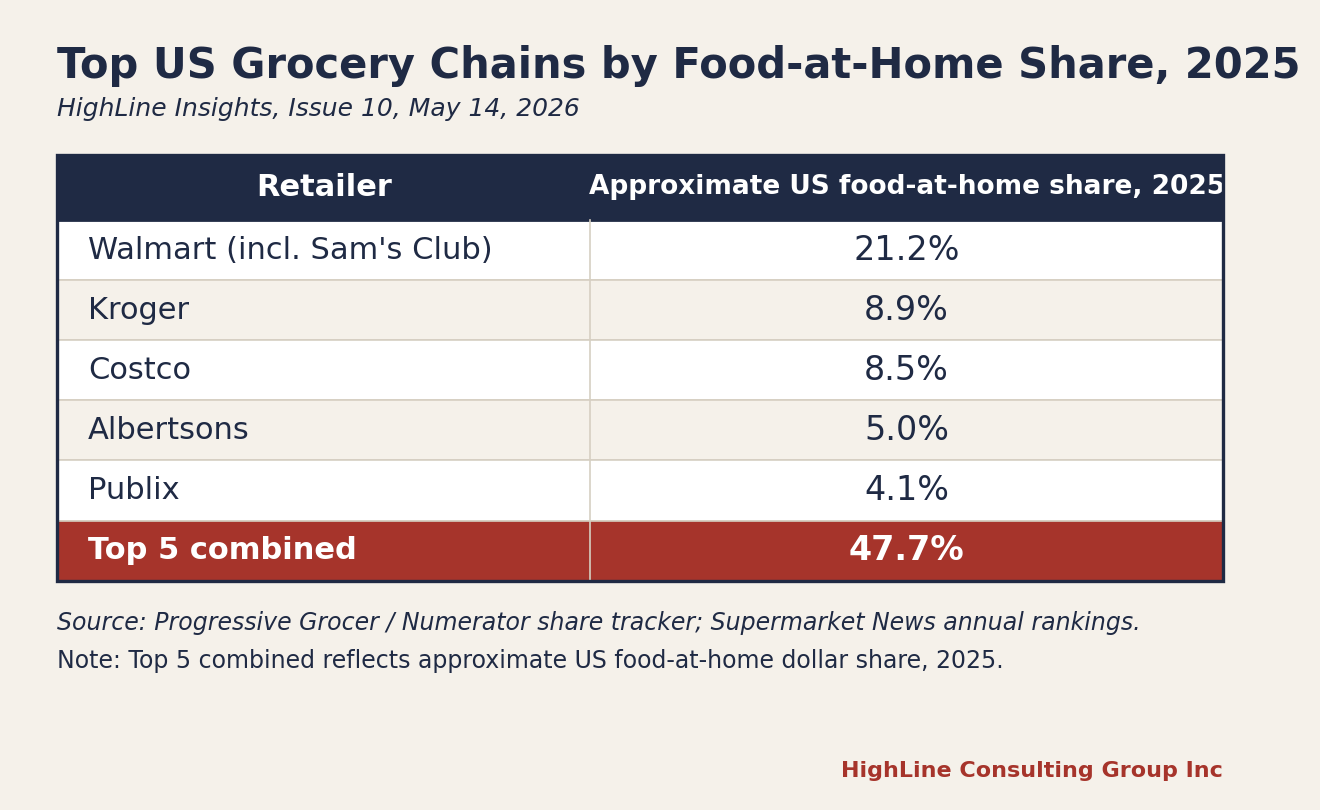

The retail concentration arc has been documented by USDA ERS itself. The Economic Research Service report A Disaggregated View of Market Concentration in the Food Retail Industry (ERR-314) traces the rising share of food retail sales captured by the largest firms. The CR4 share of United States food retailing rose from 31 percent in 2012 to 34 percent in 2019. The top 20 firms captured 65.1 percent of total food sales by 2019, up from 35.0 percent in 1990. The trend has continued in trade-press tracking using Numerator panel data and Circana point-of-sale data since.

The single largest United States grocery account, by national share, is Walmart (including Sam’s Club), at approximately 21.2 percent of the 2025 Numerator panel. The fresh beef share is likely above the all-grocery share, because Circana data show traditional supermarkets lost more than three percentage points of meat sales share between 2019 and 2023, while supercenters such as Walmart and Target gained 2.2 points of meat share over the same window. Trade reporting consistently identifies Walmart as the single largest United States fresh beef account.

The rest of the top five comes from a tighter cluster. The combined top five share of United States food-at-home sales is approximately as follows.

|

|

Source: Progressive Grocer / Numerator share tracker, Supermarket News annual rankings.

|

The next tier (Ahold Delhaize USA, H-E-B, Aldi, Target) each sits in the 2 to 4 percent range. Note the December 10, 2024 ruling from the United States District Court for Oregon enjoining the proposed Kroger-Albertsons merger, and the parties’ termination of the deal the following day. Albertsons remains an independent public company. The top five combined share would have been materially higher had the merger closed.

One data gap that deserves an honest flag. A precise top-five retailer share of United States fresh beef volume is not publicly disclosed. Circana, Numerator, and 210 Analytics sell that cut of data to retailers and processors but do not publish account-level shares. We use the all-grocery top-5 share, approximately 48 percent, as the closest defensible proxy. The directional point holds either way: retail concentration is meaningful, it has been rising for three decades, and it sits outside the explicit frame of the May 4 announcement.

3. The Pass-Through Asymmetry

This section is the technical heart of the argument. Two layers, mechanism and empirics.

The mechanism is documented in peer-reviewed work by Glynn Tonsor and coauthors at Kansas State University. Only about 50 percent of retail beef cost is the wholesale beef itself. The remainder is retail marketing services, labor, refrigeration, shrinkage, advertising, and margin. That ratio matters for any policy claim about consumer relief from a packer-side intervention, because it sets a structural ceiling. A 50 percent wholesale decline mechanically translates to at most a 25 percent retail decline, all else equal. Even a hypothetical full packer breakup, delivering an idealized wholesale price reset, would deliver only partial shelf-price relief.

The empirical layer is the asymmetric pass-through finding. Published work using BLS-based retail series, including the long literature on vertical price transmission in meat markets indexed on IDEAS/RePEc, documents that retail beef prices respond faster and more fully to wholesale increases than to wholesale decreases. Retailers raise the case price quickly when boxed beef rises. They lower the case price slowly, or hold it flat, when boxed beef falls. The gap between those two speeds is the operative source of the spread widening in the ERS series above.

The mechanism is straightforward in category management terms. A grocery chain sets the case price on a category basis, not a per-pound basis tied to the daily cutout. Once the shelf price reaches a new level the consumer accepts, the retailer has no operational incentive to retreat ahead of competitive pressure. The market discipline that would compress the spread is downstream competitive intensity at the channel level, not upstream packer behavior. In a retail tier where the top five chains hold 48 percent of food-at-home volume, that downstream competitive intensity is structurally muted.

|

Once the shelf price reaches a new level the consumer accepts, the retailer has no operational incentive to retreat ahead of competitive pressure.

|

The USDA ERS Meat Price Spreads dataset is the canonical retail-margin proxy, and the 2020 through 2026 YTD evidence is precisely what you would expect to see if the retail channel were capturing a structural rents shift, not a transient one. The 2022 print, in which the cutout fell and retail rose, is the cleanest single year to study. The April 2026 YTD print, with the spread at $3.88 per pound, is the most recent confirmation that the post-2020 widening has not reversed.

4. What This Means for the May 4 Frame

The packer tier is in losses, the producer tier is at records, the wholesale-to-retail spread has widened structurally since 2020, and the retail tier is the only operator whose pricing decisions actually impact the consumer at the case. A DOJ inquiry that names four packers while treating retail as a neutral conduit is not describing the system that sets the shelf price.

Packer concentration is higher than retailer concentration on the CR4 metric. That is not in dispute. The point is that concentration exists at multiple levels of the chain, retail concentration has risen materially over three decades, and the empirical record on the recent spread widening points at retail rather than slaughter and fabrication. The structural answer to where consumers are paying the premium is at the case. The structural answer to which tier has the market power to hold that premium even when the upstream tier softens is the retail chain.

We do not put this forward to score a partisan point. We put it forward because the DOJ investigation, and subsequent taxpayer dollars, if it is going to deliver consumer relief on beef, has to be pointed at the tier where the consumer dollar actually lands, which USDA ERS data has already solved for. Maybe the USDA and DOJ should spend time acting on prior conclusions rather than the political theater of perpetuating mid-term election campaign talking points.

|

Reader Question

If you sit anywhere in the protein supply chain, we want your read, and we want it pointed. Where is your category seeing retail margins expand against falling wholesale? Which retail account is most aggressive on shelf price discipline in your channel? If Walmart is setting the floor on fresh beef pricing in your region, say so. If a regional chain is the one holding margin while wholesale softens, name it. Reply to this email or message Michael directly. We will compile the responses for a future Shadow Issues report.

|

|