|

Beef has owned the headlines for months now, so let’s give chicken its turn. The complex is doing something in 2026 that has genuinely surprised the trade, and it is worth a few minutes of your attention.

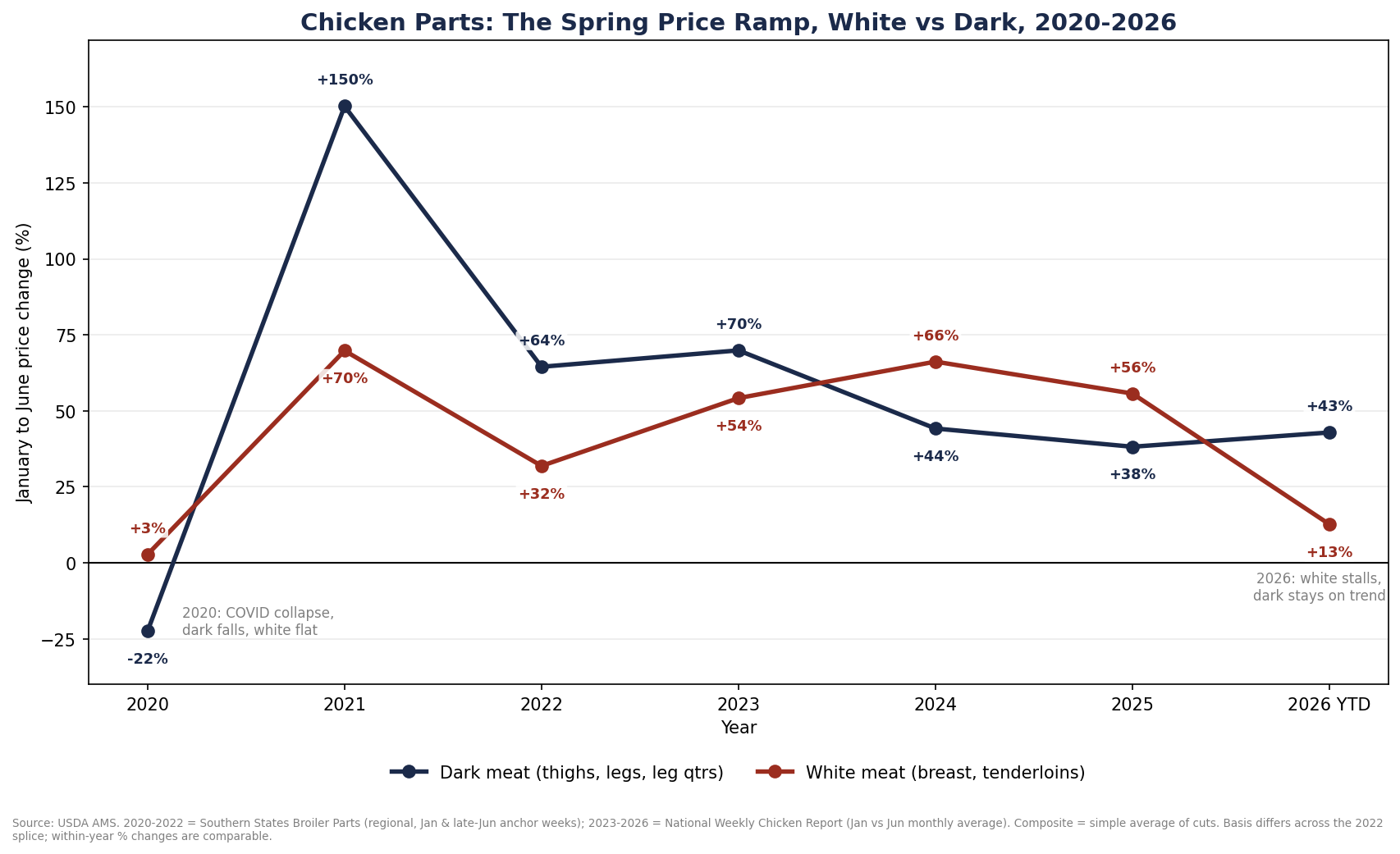

Start with the pattern that usually holds. Every spring, the chicken complex runs the same play: prices climb from January into June as grilling season demand builds. From 2021 through 2025, that pull lifted both white and dark cuts without fail. The white meat composite, boneless skinless breast and tenderloins, gained anywhere from 32 to 70 percent off its January base. The only break in the streak was 2020, when the COVID foodservice collapse dragged dark and export cuts sharply lower while white held roughly flat. The spring ramp is one of the more reliable patterns in the protein industry.

This year broke that pattern, and it broke from the side nobody was expecting. Through early June, boneless skinless breast is up just 6 percent and tenderloins 19 percent. That makes this the weakest spring in our seven-year record, softer even than the 2020 shock. Dark meat, meanwhile, did exactly what dark meat does: boneless skinless thighs are up 49 percent, bone-in legs 55 percent, and bulk leg quarters 24 percent, all squarely range bound.

|

|

Chicken white meat versus dark meat pricing, 2020 to 2026. Source: HighLine Consulting Group analysis.

|

Step back and it starts to make sense. Breast meat has run through two of its highest pricing spikes on record in the last four years, and those spikes forced culinary teams to get creative with dark meat. That shift has been building for a while, and it kept building this year, arguably at the expense of breast and tenderloin movement. The result is a compressing white-to-dark meat spread: breast has barely budged from January’s $1.29 to roughly $1.37, while boneless skinless thighs have climbed to $2.02. In a normal year, white meat climbs alongside dark meat or leads it outright. This spring, white meat stalled while dark meat kept on trajectory.

I want to be careful about the why. The data confirms the divergence; it does not fully explain it. A few forces are clearly in the mix. Bird health and overall supply have run stronger than expected. At the same time, a soft U.S. dollar has pulled export demand higher, and dark meat demand, boneless skinless thigh meat especially, has stayed strong on its own merits.

For buyers, the signal is concrete. This spring, white meat is the value story, not the cost-pressure story. Any coverage strategy built around the usual breast-led rally is positioned for a market that simply has not shown up this year. Expect the typical second-half softening in white meat pricing, but do not count on it running far below where we sit today. And if three decades of watching these markets have taught me anything, it is this: 2027 will likely adjust higher as production responds to supply and demand signals, right as fertilizer costs catch up to feed inputs.

If this is the kind of read you want every week, HighLine Insights Pro was built for you. The new offering launches June 23 and delivers deeper data like this to members on a weekly basis. Members also get early access to our quarterly deep-dive reports, a full 30 days before they go live on the web.

|