Wrong Investigation, Wrong Target

On May 4, 2026, the Department of Justice announced an antitrust investigation into the Big Four beef packers. It is the second such probe in five years. The first one was opened in 2020 and closed in 2025 without charges.

The press conference framed the action as producer and consumer protection. The data say the framing has the wrong target.

Across the last ten quarters, the publicly measurable Big Four packers are absorbing billions of dollars in beef segment losses, not profits. Cow-calf producers are posting the strongest margins in the recorded history of the industry. The United States beef cow herd is at its lowest level since 1961. The wholesale-to-retail beef spread has roughly quadrupled in nominal terms since 2000. The investigation is pointed at the wrong tier of the supply chain.

We do not assume bad faith on the part of the Department. We do read the public record. Over the next two days we lay it out.

Part 1, today, covers five things. The news hook and what the Agri Stats settlement does and does not prove. The packer financial record, anchored in the SEC filings. The Packers and Stockyards Act, the century-old statute that already covers the conduct in question. Argentina, the live policy experiment that already ran this playbook to its conclusion. And the cow-calf data on the producers the investigation purports to defend.

Part 2, tomorrow, runs alongside the regular HighLine Insights sections and covers where the consumer dollar actually lands. The USDA Economic Research Service wholesale-to-retail spread series and the structure of United States grocery retail concentration.

The Agri Stats Hook and What It Does and Does Not Prove

The DOJ’s choice of moment was not random. On May 8, 2026, four days after the press conference, the Department announced a proposed consent decree resolving its September 2023 civil antitrust complaint against Agri Stats, Inc., the Indiana-based agricultural data and benchmarking service that for decades collected and redistributed competitively sensitive production, cost, and pricing data among the country’s largest broiler chicken, pork, and turkey processors. The original complaint, filed in the District of Minnesota, alleged a Section 1 Sherman Act violation through an information-exchange architecture that the Department argued enabled tacit coordination on output, pricing, and capacity. Four states, Minnesota, California, Colorado, and North Carolina, later joined.

The Agri Stats settlement is structural, not monetary. There is no civil penalty against Agri Stats in the DOJ resolution. The decree prohibits offering sales report books, bars identification of contributing companies and publication of company rankings, mandates an antitrust compliance program, and installs a court-appointed monitor with oversight authority for up to seven years. Agri Stats is required to make its reports available to any United States individual or business on terms at least as favorable as those offered to meat processors.

|

The strongest information-sharing antitrust case the Department has built ended in a structural consent decree, not a finding of overt price fixing.

|

That is a meaningful precedent, and it does not extend automatically to fed cattle. The Agri Stats case did not include a beef component. The Department has not publicly alleged that the Big Four beef packers were Agri Stats subscribers on the cattle side at anything resembling the scope established for chicken, pork, and turkey.

At the May 4 press conference, Director Navarro used the Agri Stats resolution as a rhetorical pivot from poultry and pork into beef. On the record, he said:

|

“These folks are now aware and they’re going to be hypersensitive to any kind of things that they might pull. Across the meat and other issues of the ag sector, they’re going to start behaving better. That’s not going to forgive what they’ve done in the past, but these kind of actions create benefits in and of themselves as the investigation goes forward.”

— Director Peter Navarro, DOJ Antitrust Announcement press conference, May 4, 2026.

|

We are not putting that quotation forward to score a point. We are putting it forward because it captures the gap between the rhetoric and the data. The “behaving better” formulation presumes prior misbehavior. The evidentiary record from the most recent five-year prior beef probe is that the Department reviewed the same industry, drew the same complaints, opened the same questions, and closed the file without charges. That is the answer the prior administration reached after a full review. The question for the current investigation is not whether to ask the questions again. The question is what new evidence justifies a different answer, and the press conference did not produce one.

What the SEC Filings Say About Packer Profits

The fastest test of the populist intuition that packers are profiteering on beef is the SEC filings. The Tyson Foods Beef segment is the cleanest available read. Tyson’s fiscal year ends the Saturday closest to September 30. The Beef segment operating result is disclosed each quarter in the 8-K earnings release filed as Exhibit 99.1 on EDGAR, cross-checked against the annual 10-K. The table below reports GAAP operating income or loss, not a non-GAAP adjusted figure, across the last ten quarters.

| Tyson Fiscal Quarter |

Period Ending |

Beef Op. Income (Loss), USD M, GAAP |

| Q1 FY2024 | Dec 30, 2023 | (206) |

| Q2 FY2024 | Mar 30, 2024 | (35) |

| Q3 FY2024 | Jun 29, 2024 | (69) |

| Q4 FY2024 | Sep 28, 2024 | (71) |

| Q1 FY2025 | Dec 28, 2024 | (64) |

| Q2 FY2025 | Mar 29, 2025 | (258) |

| Q3 FY2025 | Jun 28, 2025 | (494) |

| Q4 FY2025 | Sep 27, 2025 | (319) |

| Q1 FY2026 | Dec 27, 2025 | (319) |

| Q2 FY2026 | Mar 28, 2026 | (240) |

| Ten-quarter aggregate | | $(2,075) M |

Source: Tyson Foods 8-K Exhibit 99.1 quarterly press releases, SEC EDGAR (CIK 0000100493). Cross-check: the FY2025 10-K reports Beef segment GAAP operating loss of $(381) million for FY2024 and $(1,135) million for FY2025, which match the press-release sums.

The cumulative figure is roughly $2.08 billion in GAAP operating losses across ten quarters at a single one of the Big Four. The trajectory is not flat. It is accelerating. The two heaviest single-quarter losses, $(494) million in Q3 FY2025 and tied $(319) million prints in Q4 FY2025 and Q1 FY2026, all sit in the most recent five quarters, the period in which retail beef prices reached record highs.

JBS S.A. and Marfrig National Beef post the same pattern in their own filings. JBS Beef North America swung from positive $247 million in Adjusted EBITDA in FY2024 to a $319.5 million loss in FY2025 on record revenue, a $566 million year-over-year deterioration. Marfrig National Beef fell 40 percent in FY2024 and turned to a quarterly loss in Q1 2025. Cargill is privately held, does not file segment financials with the SEC, and is excluded per HighLine’s standing sourcing rule.

A profiteering thesis cannot survive contact with the SEC filings. If the Big Four were extracting structural rents from elevated retail beef prices, the disclosed segment results would show profit expansion, not the steepest losses in the recent record. They do not.

The Statute That Already Covers This

The Packers and Stockyards Act of 1921, codified at 7 U.S.C. sections 181 through 229c, has vested broad federal authority over unfair and anticompetitive conduct by packers, dealers, and live poultry dealers for more than a century. The substantive prohibition at 7 U.S.C. Section 192 reaches deceptive practice, undue preference, supply apportionment, monopolization, conspiracy, and, in subsection (d), “the buying or selling of any article for the purpose or with the effect of manipulating or controlling prices.” That is the conduct the current investigation contemplates. The Department does not need a new statute to address it.

Authority is not the issue. The Secretary of Agriculture has rulemaking power under Section 228, temporary injunction authority under Section 228a, and civil penalty authority under Section 193 and Section 213. The USDA Packers and Stockyards Division inside the Agricultural Marketing Service has investigative jurisdiction today, and it works alongside the Department on overlapping conduct when DOJ chooses to step in. Another taxpayer-funded DOJ investigation is not what the framework requires. Enforcement priority and rule durability are what the framework requires, and the post-2008 rulemaking cycle, which has cycled through four administrations, shows the binding constraint sits there.

The Five Rivers Cattle Feeding history is the recent example of why the century-old statute is enough. In October 2008, JBS S.A. completed its acquisition of Smithfield Beef Group, which included 100 percent of Five Rivers Ranch Cattle Feeding LLC, then the largest cattle-feeding operation in the United States with capacity near 811,000 head. A packer owning the largest fed-cattle feedlot in the country raised exactly the kind of market-access and undue-preference concern Section 192(b) is built to reach. JBS divested Five Rivers on January 5, 2018, with Pinnacle Asset Management acquiring the eleven feedyards for $200 million paired with a long-term supply agreement to JBS USA plants. The structural concern was real, and it was resolved inside the existing framework without a new statute, a structural breakup of the packing sector, or a high-profile DOJ press conference.

The question for the current Department is not whether to write new law. The question is whether the conduct alleged in beef rises to the standard the law already contains. The 2020 to 2025 prior probe that closed without charges suggests the answer the prior administration reached after a full review.

The Policy Endgame Has Been Run Already: Argentina

The political logic of the current framing, restrictions on packer scale and export limits in the name of consumer protection, has been run as a live policy experiment. Argentina ran it for nearly two decades. Successive administrations imposed beef export bans, export taxes, and quota regimes to keep domestic prices down. The results are a matter of public record:

- Argentina fell from the world’s number-three beef exporter in 2005, at roughly 700,000 tons, to number eleven by 2014, at roughly 200,000 tons.

- The national cattle herd contracted by roughly 10 million head between 2007 and 2012.

- Approximately 20 percent of beef packers closed or suspended operations.

- Ranchers liquidated herds and converted pasture to soybeans.

- Domestic cattle prices rose 300 percent despite the policy aim of cheaper beef, because supply collapsed faster than the export channel was closed.

|

The clearest natural experiment available shows that consumer-protection framing in a beef policy context did not lower domestic prices, did not protect producers, and did not preserve packing capacity. It destroyed all three.

|

Argentina is now reversing the policy. The Milei government has let the most recent export decree expire, restored exports across all cuts, cut the beef export tax, and in 2025 lifted a 52-year live cattle export ban. The coalition that built the restrictions justified them in producer-protection and consumer-protection terms. The coalition dismantling them is acting on the evidence of what those policies actually did. The United States debate would benefit from reading the same record.

The Producers the Investigation Names Are Posting Record Margins

The political narrative animating the current investigation rests on a foundational assumption, that consolidation in beef packing has transferred value away from cow-calf producers. The data say the opposite. Cow-calf producers, the upstream cohort the investigation purports to defend, are posting the strongest margins in the recorded history of the industry. They are doing so for the textbook reason: the United States beef cow herd is at its lowest level since 1961, calf supply is structurally short, and a short supply commands a high price. This is a cattle cycle, not a conspiracy.

Three independent lines of evidence converge on that conclusion.

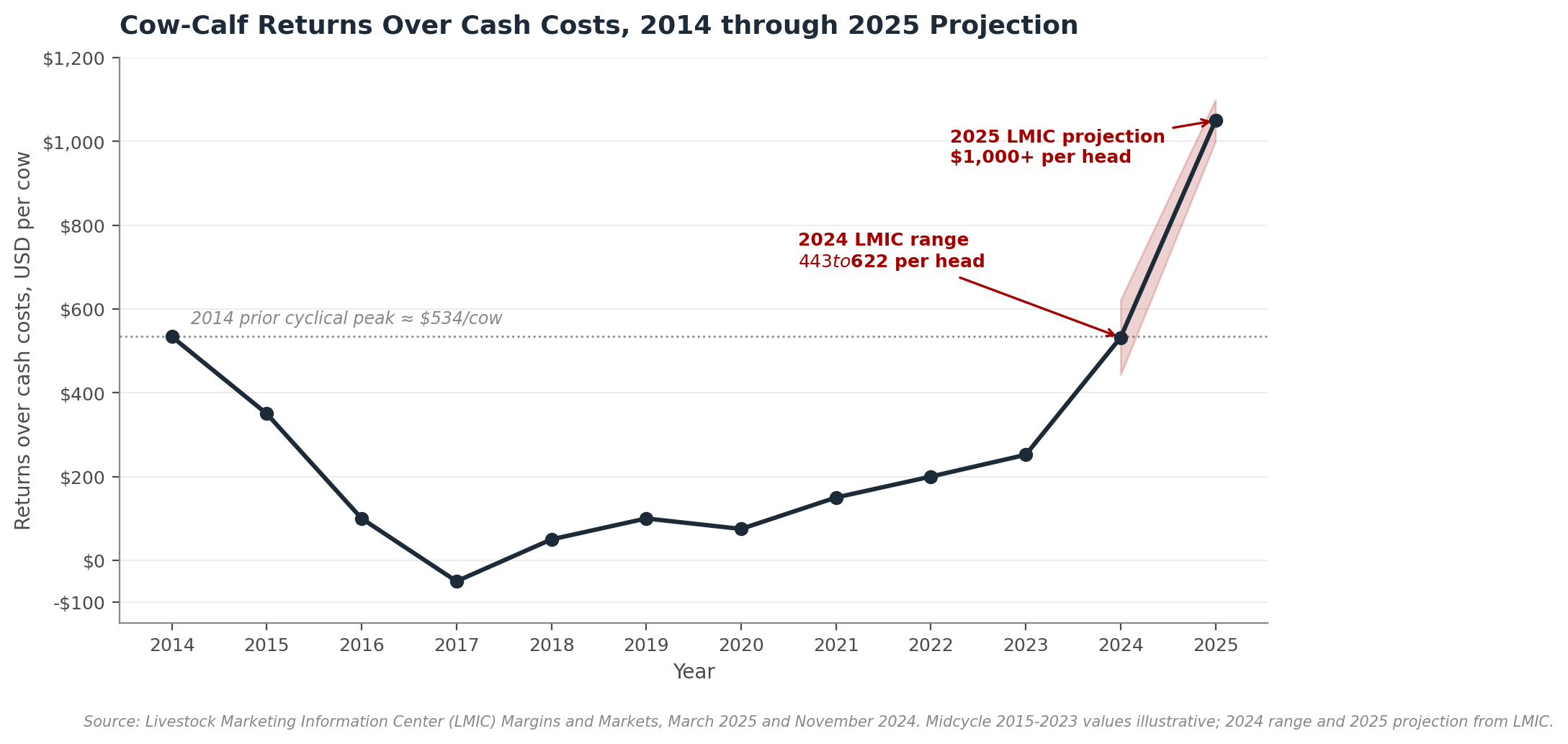

First, cow-calf returns over cash costs. The Livestock Marketing Information Center maintains the industry-standard series. The chart below shows the trajectory across the last decade.

|

|

Cow-calf returns over cash costs, 2014 through 2025 projection. Source: LMIC Margins and Markets.

|

The 2014 cyclical peak printed near $534 per cow. Margins compressed through the back half of the 2010s and re-expanded as the herd contracted. The 2024 LMIC range of $443 to $622 per cow already exceeds the prior nominal record on the upper end. The 2025 LMIC projection sits above $1,000 per head, an unambiguous nominal record. USDA ERS Commodity Costs and Returns confirms the cost backdrop, with 2025 forecasted operating costs plus pasture rent near $1,059 per head against calf revenue running near or above $1,600 per head.

Second, beef-on-dairy day-old calf prices. This is the cleanest natural experiment in the United States cattle complex because the day-old beef-on-dairy crossbred calf is a category of animal that packers do not buy at that stage. The progression speaks for itself.

| Period |

Approximate Day-Old Beef-on-Dairy Calf Price |

| Circa 2020 | ~$85 per head |

| 2023 to 2024 | $400 to $800 per head |

| April 2026 | $1,500 to $1,800 regionally (PA ~$1,800; Midwest ~$1,500 to $1,600; Jersey crosses ~$1,300) |

| 2026 outlook | $1,500 to $1,750 sustained |

Sources: FinancialContent (April 13, 2026); Red River Farm Network (March 21, 2026); Lancaster Farming; Hoard’s Dairyman; Penn State Extension.

The implied multiple from roughly $85 to roughly $1,650 over six years is more than nineteenfold. There is no plausible packer-conspiracy theory that explains a price increase on a category of animal that packers do not buy at the day-old stage. The explanation is structural. Feeder cattle scarcity, dairy producer adoption of beef genetics on the bottom tier of their herd, and downstream demand for any feeder animal that can be finished. Beef-on-dairy now contributes roughly 20 percent of United States beef production.

Third, the herd itself. USDA NASS released its January 1, 2026 cattle inventory on January 30, 2026. The figures are these. All cattle and calves at 86.2 million head, the smallest total United States herd since 1951. Beef cows at 27.6 million head, down 1 percent year over year and the lowest level since 1961. Milk cows at 9.57 million head, up. 2025 calf crop at 32.9 million head, down 2 percent. Cattle on feed at 13.8 million head, down 3 percent. Even with 2025 beef cow slaughter down more than 500,000 head, the breeding herd contracted further. Producers are holding back heifers, which is to say they are responding to the price signal, but the lag from heifer retention to weaned calf is roughly two years. The supply tightness will continue to support upstream prices through at least 2027.

The cohort the investigation is framed as defending is, on the evidence, the cohort benefiting most from the current market structure. A policy framework predicated on producer harm cannot be reconciled with producers receiving the highest real prices in decades for the calves they sell.

What We Have Established, and What Comes Tomorrow

The packer-segment financial record across the last ten quarters is one of accelerating losses, not extraction. Tyson Foods alone has logged a cumulative $(2,075) million GAAP operating loss in Beef. JBS and Marfrig National Beef show the same pattern in their own filings.

The cow-calf segment record is the inverse. LMIC projects 2025 returns above $1,000 per head, beef-on-dairy day-old calf prices have risen more than nineteenfold since 2020, and the United States beef cow herd is at the lowest level since 1961 on the back of a 75-year supply low across all cattle and calves.

The Packers and Stockyards Act already covers the conduct the Department is investigating. Section 192 reaches price manipulation and undue preference directly. USDA has the authority to act today. The Five Rivers history shows that structural concerns can be resolved inside the existing framework. The 2020 to 2025 prior probe closed without charges after a five-year review.

The closest historical analog of the policy direction the rhetoric points toward is Argentina, where the same framing did not lower prices, did not protect producers, and did not preserve packing capacity. It destroyed all three.

|

Coming Tomorrow

Part 2 publishes alongside the regular HighLine Insights sections. Where the consumer dollar actually goes. The USDA ERS Meat Price Spreads dataset shows the wholesale-to-retail beef spread has roughly quadrupled in nominal terms since 2000, from $0.94 per pound to $3.39 per pound in 2025, with the most aggressive widening since 2020. The United States grocery retail tier is itself concentrated, with the top five chains controlling roughly 48 percent of food-at-home sales. Part 2 also brings in industry perspectives to complement the data with the operating reality behind it.

|

|